9706_m25_er

💡 Premium Overlay Enabled

Cambridge International Advanced Subsidiary and Advanced Level

9706

Ac

c

ounting

March

20

2

5

Princip

a

l Examiner Report for Teachers

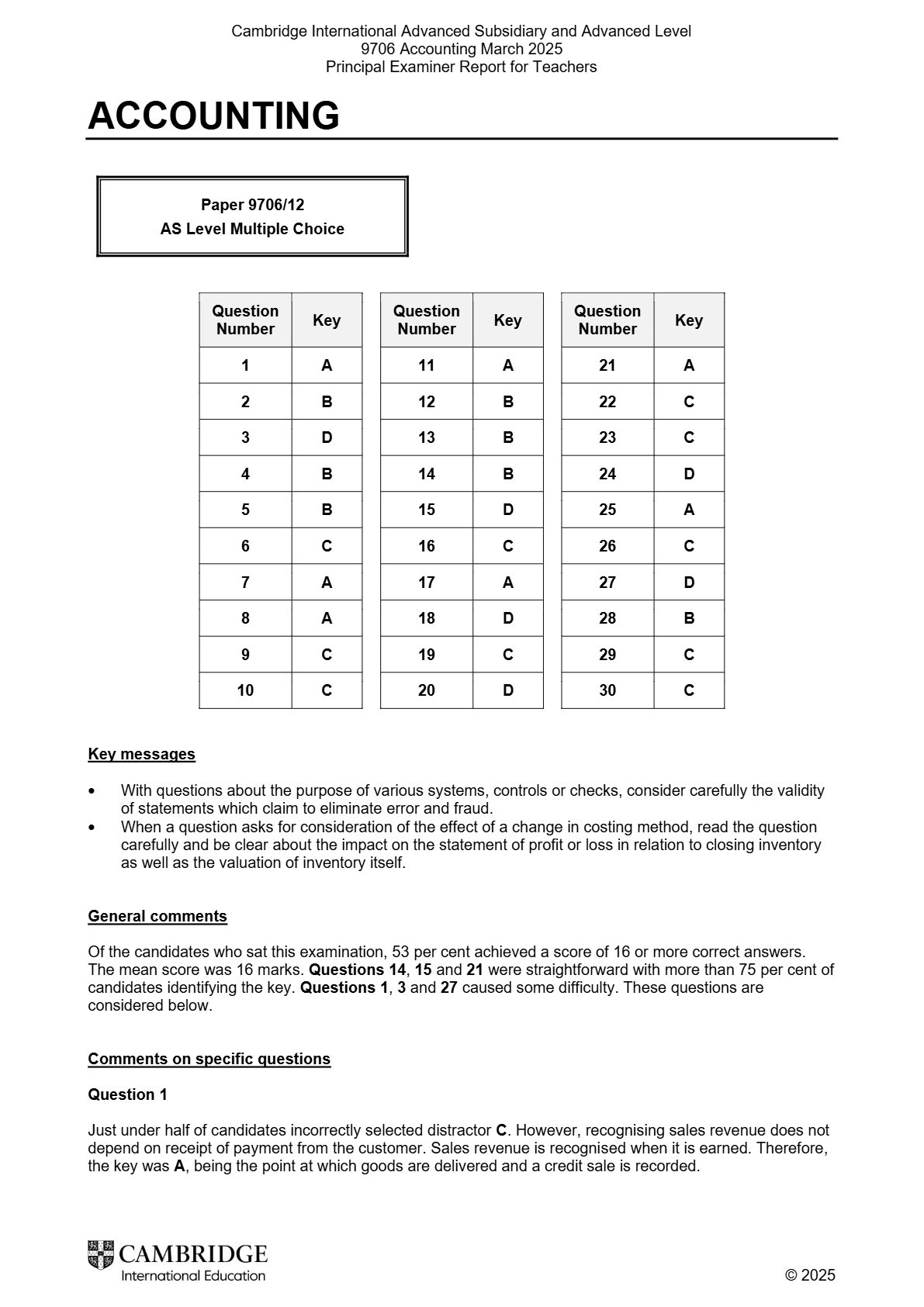

ACCOUNTING

Paper

9706

/

12

AS Level Multiple Choice

Question

Question

Question

Key

Key

Key

Number

Number

Number

1

A

11

A

21

A

2

B

12

B

22

C

3

D

13

B

23

C

4

B

14

B

24

D

5

B

15

D

25

A

6

C

16

C

26

C

7

A

17

A

27

D

8

A

18

D

28

B

9

C

19

C

29

C

10

C

20

D

30

C

Key messages

•

With questions about the purpose of various systems, controls or checks, consider carefully the validity

of statements which claim to eliminate

error and fraud.

•

When a question asks for consideration of the effect of a change in costing method, read the question

carefully and be clear about the impact on the statement of profit or loss in relation to closing inventory

as well as the valuation of inventory itself.

General comments

Of the candidates who sat this examination, 53

per cent

achieved a score of 16 or more correct answers.

The mean score was 16 marks.

Questions 14

,

15

and

21

were straightforward with more than 75

per cent

of

candidates identifying the key.

Questions 1

,

3

and

27

caused some difficulty. These questions are

considered below.

Comments on specific questions

Question 1

Just under half of candidates incorrectly selected distractor

C

. However, recogni

s

ing sales revenue does not

depend on receipt of payment from the customer. Sales revenue is recogni

s

ed when it is earned.

Therefore,

the key was

A

, being the point at which goods are delivered and a credit sale is recorded.

©

20

2

5

Cambridge International Advanced Subsidiary and Advanced Level

9706 Ac c ounting March 20 2 5

Princip a l Examiner Report for Teachers

ACCOUNTING

Paper 9706 / 12

AS Level Multiple Choice

Question Question Question

Key Key Key

Number Number Number

1 A 11 A 21 A

2 B 12 B 22 C

3 D 13 B 23 C

4 B 14 B 24 D

5 B 15 D 25 A

6 C 16 C 26 C

7 A 17 A 27 D

8 A 18 D 28 B

9 C 19 C 29 C

10 C 20 D 30 C

Key messages

• With questions about the purpose of various systems, controls or checks, consider carefully the validity

of statements which claim to eliminate error and fraud.

• When a question asks for consideration of the effect of a change in costing method, read the question

carefully and be clear about the impact on the statement of profit or loss in relation to closing inventory

as well as the valuation of inventory itself.

General comments

Of the candidates who sat this examination, 53 per cent achieved a score of 16 or more correct answers.

The mean score was 16 marks. Questions 14 , 15 and 21 were straightforward with more than 75 per cent of

candidates identifying the key. Questions 1 , 3 and 27 caused some difficulty. These questions are

considered below.

Comments on specific questions

Question 1

Just under half of candidates incorrectly selected distractor C . However, recogni s ing sales revenue does not

depend on receipt of payment from the customer. Sales revenue is recogni s ed when it is earned. Therefore,

the key was A , being the point at which goods are delivered and a credit sale is recorded.

© 20 2 5

Cambridge International Advanced Subsidiary and Advanced Level

9706

Ac

c

ounting

March

20

2

5

Princip

a

l Examiner Report for Teachers

Question 3

More candidates selected distractor

B

than the key, which was

D

. The question required a careful reading of

the options. A computerised accounting system can only assist in the process of minimising errors by using

various automated calculations and

checks but

cannot ensure that the records will be completely error free.

Question 27

Many candidates opted for distractor

C

. This correctly identified that the value of inventory would increase

using absorption costing,

however,

it

did not identify the correct effect on profit for the year. This was the first

year of trading for the business, therefore the inventory valuation relates to closing inventory. A higher value

of closing inventory would reduce the cost of sales and hence in

crease profit for the year.

Thus

,

the key was

D

.

©

20

2

5

Cambridge International Advanced Subsidiary and Advanced Level

9706 Ac c ounting March 20 2 5

Princip a l Examiner Report for Teachers

Question 3

More candidates selected distractor B than the key, which was D . The question required a careful reading of

the options. A computerised accounting system can only assist in the process of minimising errors by using

various automated calculations and checks but cannot ensure that the records will be completely error free.

Question 27

Many candidates opted for distractor C . This correctly identified that the value of inventory would increase

using absorption costing, however, it did not identify the correct effect on profit for the year. This was the first

year of trading for the business, therefore the inventory valuation relates to closing inventory. A higher value

of closing inventory would reduce the cost of sales and hence in crease profit for the year.

Thus , the key was D .

© 20 2 5

Cambridge International Advanced Subsidiary and Advanced Level

9706

Accounting

March

20

2

5

Princip

a

l Examiner Report for Teachers

ACCOUNTING

Paper

9706

/

22

AS Level Fundamentals of Accounting

Key messages

C

andidates provided detailed, often well developed, responses to the two questions requiring an evaluation

and

performed well on

these two questions. However, there are still areas of concern:

•

Candidates must show workings in the appropriate areas within the boxes provided. This ensures that

partial marks can be awarded if the final answer is incorrect.

•

A common weakness was a failure to use correct narratives in ledger accounts. This was noticeable in

the preparation of the sales ledger control account, and the ordinary share capital and reserve accounts

of the limited company. Balances must always be br

ought down on any ledger accounts prepared.

•

Abbreviations should not be used and the date columns used appropriately.

Comments on specific

questions

Question 1

The question concentrated on the financial statements of a partnership.

(a)

A draft profit had to be corrected to reflect corrections

to

arrive at a revised profit for the year.

Many

gained full marks to start this

paper,

and calculations clearly indicated whether items were added or

subtracted from the draft profit for the year.

The main weaknesses were a failure to calculate

interest on the partner’s loan taking account of the fact that the loan had been arranged part way

through the year, and that the goods taken for own use by the owner would increase, rather than

decrease

, the draft profit for the year.

(b)

A partnership appropriation account was required

. It

is essential that the full names of the partners

are used and not their initials. Few candidates gained full marks as the interest on drawings was

incorrect

in many cases

. The rest was well done and gained the

marks,

and the layout was

generally good.

However, most

candidates failed to take account of the additional drawings when

calculating interest on drawings in the appropriation account. It is essential that when a loss is

calculated

it is labelled as a loss and not as a profit. A common

extraneous element

in this account

was the interest on partner loan or the actual loan itself which then meant the share of residual loss

mark could not be awarded.

(c)

Few candidates prepared the current account correctly as in many cases

the drawings were

either

incorrect or not totalled. The remainder of the account was generally well done with a good layout

and labels. Some candidates did confuse the two partners.

(d)

An extract of the capital and liabilities section from the statement of financial position was required

and few candidates

performed well on this question

. The partner loan

, in many cases,

was

incorrectly

labelled as a bank loan. The current liabilities were often incomplete. The layout was

generally good and most appropriately labelled the sections and they were in the correct order.

Only

a minority of candidates remembered that a partner had increased her capital during the year

when preparing the ex

tract.

©

20

2

5

Cambridge International Advanced Subsidiary and Advanced Level

9706 Accounting March 20 2 5

Princip a l Examiner Report for Teachers

ACCOUNTING

Paper 9706 / 22

AS Level Fundamentals of Accounting

Key messages

C andidates provided detailed, often well developed, responses to the two questions requiring an evaluation

and performed well on these two questions. However, there are still areas of concern:

• Candidates must show workings in the appropriate areas within the boxes provided. This ensures that

partial marks can be awarded if the final answer is incorrect.

• A common weakness was a failure to use correct narratives in ledger accounts. This was noticeable in

the preparation of the sales ledger control account, and the ordinary share capital and reserve accounts

of the limited company. Balances must always be br ought down on any ledger accounts prepared.

• Abbreviations should not be used and the date columns used appropriately.

Comments on specific questions

Question 1

The question concentrated on the financial statements of a partnership.

(a) A draft profit had to be corrected to reflect corrections to arrive at a revised profit for the year. Many

gained full marks to start this paper, and calculations clearly indicated whether items were added or

subtracted from the draft profit for the year. The main weaknesses were a failure to calculate

interest on the partner’s loan taking account of the fact that the loan had been arranged part way

through the year, and that the goods taken for own use by the owner would increase, rather than

decrease , the draft profit for the year.

(b) A partnership appropriation account was required . It is essential that the full names of the partners

are used and not their initials. Few candidates gained full marks as the interest on drawings was

incorrect in many cases . The rest was well done and gained the marks, and the layout was

generally good. However, most candidates failed to take account of the additional drawings when

calculating interest on drawings in the appropriation account. It is essential that when a loss is

calculated it is labelled as a loss and not as a profit. A common extraneous element in this account

was the interest on partner loan or the actual loan itself which then meant the share of residual loss

mark could not be awarded.

(c) Few candidates prepared the current account correctly as in many cases the drawings were either

incorrect or not totalled. The remainder of the account was generally well done with a good layout

and labels. Some candidates did confuse the two partners.

(d) An extract of the capital and liabilities section from the statement of financial position was required

and few candidates performed well on this question . The partner loan , in many cases, was

incorrectly labelled as a bank loan. The current liabilities were often incomplete. The layout was

generally good and most appropriately labelled the sections and they were in the correct order.

Only a minority of candidates remembered that a partner had increased her capital during the year

when preparing the ex tract.

© 20 2 5

#cambridge#multiple-choice#accounting#may-june#exam-year