9706_m25_in_42

💡 Premium Overlay Enabled

Cambridge International AS

& A Level

ACCOUNTING

9706/42

Paper 4 Cost and Management Accounting

February/March

2025

INSERT

1 hour

* 4 4 6 3 3 2 6 4 7 8 - I *

INFORMATION

●

This insert contains all of the sources referred to in the questions.

●

You may annotate this insert and use the blank spaces for planning.

Do not write your answers

on the

insert.

This document has

4

pages. Any blank pages are indicated.

DC (PQ) 340826/2

© UCLES 2025

[Turn over

Cambridge International AS & A Level

ACCOUNTING 9706/42

Paper 4 Cost and Management Accounting February/March 2025

INSERT 1 hour

* 4 4 6 3 3 2 6 4 7 8 - I *

INFORMATION

● This insert contains all of the sources referred to in the questions.

● You may annotate this insert and use the blank spaces for planning. Do not write your answers on the

insert.

This document has 4 pages. Any blank pages are indicated.

DC (PQ) 340826/2

© UCLES 2025 [Turn over

2

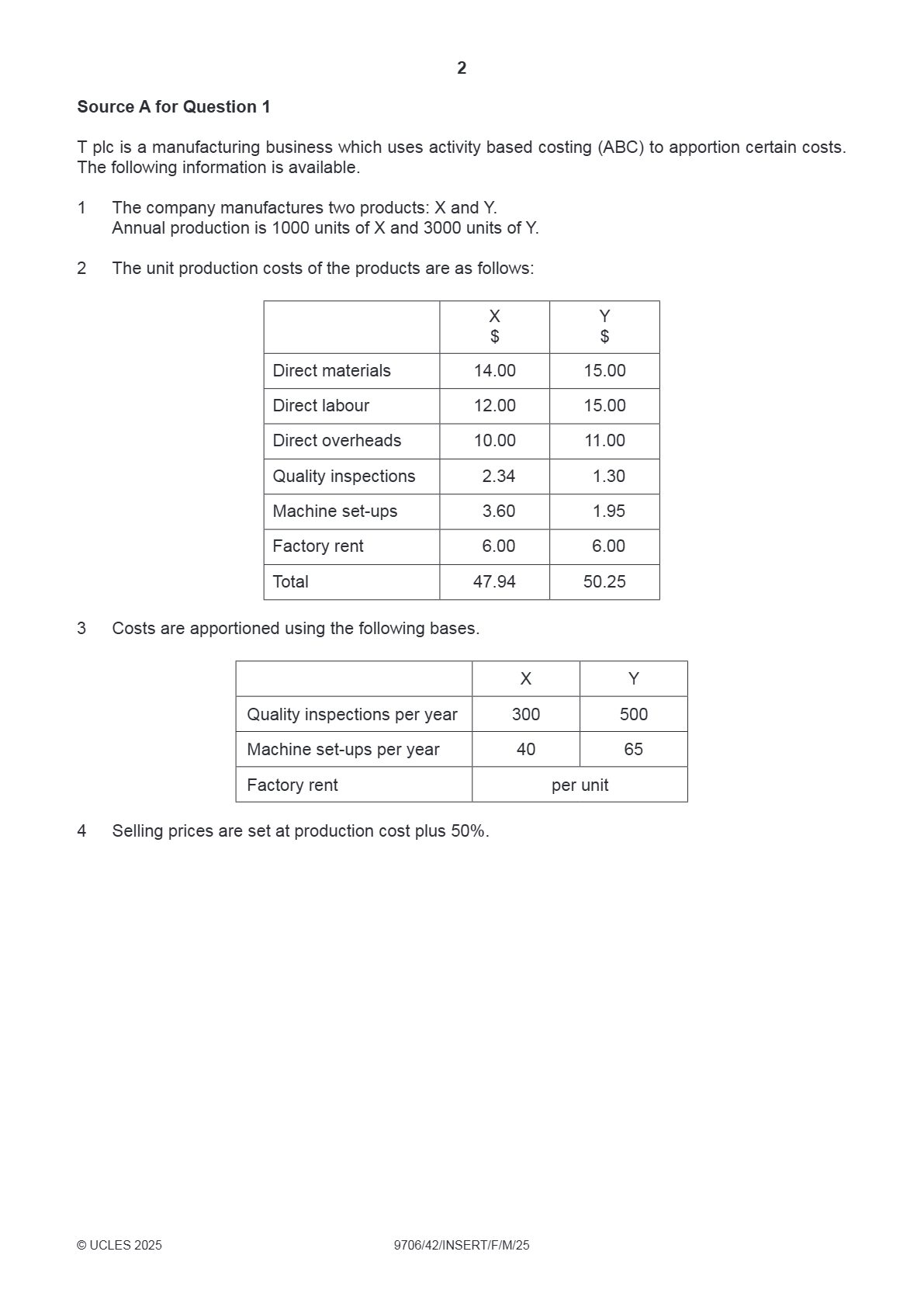

Source A for Question 1

T plc is a manufacturing business which uses activity based costing (ABC) to apportion certain costs.

The following information is available.

1

The company manufactures two products: X and Y.

Annual production is 1000 units of X and 3000 units of Y.

2

The unit production costs of the products are as follows:

X

Y

$

$

Direct materials

14.00

15.00

Direct labour

12.00

15.00

Direct overheads

10.00

11.00

Quality inspections

2.34

1.30

Machine set-ups

3.60

1.95

Factory rent

6.00

6.00

Total

47.94

50.25

3

Costs are apportioned using the following bases.

X

Y

Quality inspections per year

300

500

Machine set-ups per year

40

65

Factory rent

per unit

4

Selling prices are set at production cost plus 50%.

© UCLES 2025

9706/42/INSERT/F/M/25

2

Source A for Question 1

T plc is a manufacturing business which uses activity based costing (ABC) to apportion certain costs.

The following information is available.

1 The company manufactures two products: X and Y.

Annual production is 1000 units of X and 3000 units of Y.

2 The unit production costs of the products are as follows:

X Y

$ $

Direct materials 14.00 15.00

Direct labour 12.00 15.00

Direct overheads 10.00 11.00

Quality inspections 2.34 1.30

Machine set-ups 3.60 1.95

Factory rent 6.00 6.00

Total 47.94 50.25

3 Costs are apportioned using the following bases.

X Y

Quality inspections per year 300 500

Machine set-ups per year 40 65

Factory rent per unit

4 Selling prices are set at production cost plus 50%.

© UCLES 2025 9706/42/INSERT/F/M/25

3

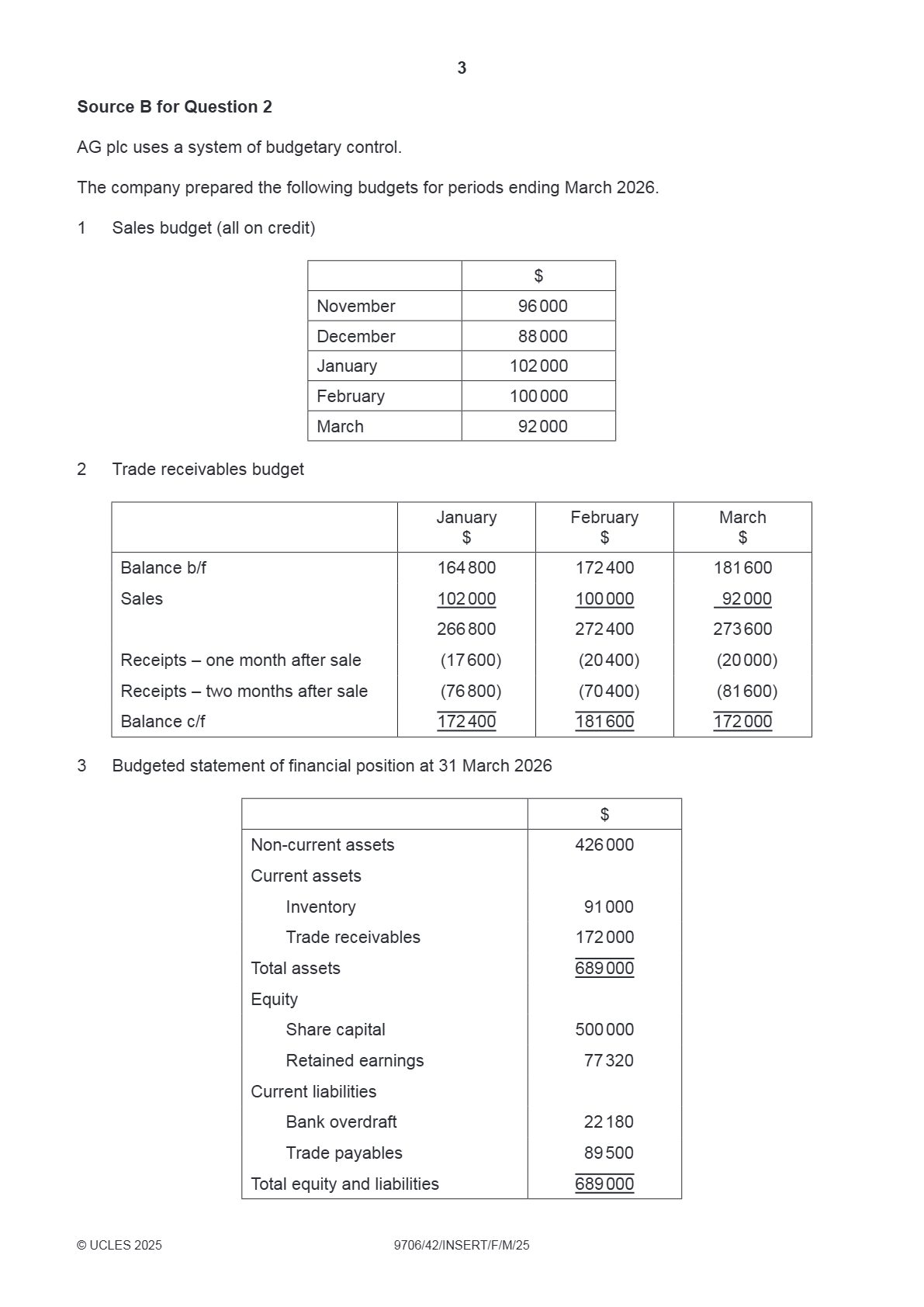

Source B for Question 2

AG plc uses a system of budgetary control.

The company prepared the following budgets for periods ending March 2026.

1

Sales budget (all on credit)

$

November

96 000

December

88 000

January

102 000

February

100 000

March

92 000

2

Trade receivables budget

January

February

March

$

$

$

Balance b/f

164 800

172 400

181 600

Sales

102 000

100 000

92 000

266 800

272 400

273 600

Receipts – one month after sale

(17 600)

(20 400)

(20 000)

Receipts – two months after sale

(76 800)

(70 400)

(81 600)

Balance c/f

172 400

181 600

172 000

3

Budgeted statement of financial position at 31 March 2026

$

Non-current assets

426 000

Current assets

Inventory

91 000

Trade receivables

172 000

Total assets

689 000

Equity

Share capital

500 000

Retained earnings

77 320

Current liabilities

Bank overdraft

22 180

Trade payables

89 500

Total equity and liabilities

689 000

© UCLES 2025

9706/42/INSERT/F/M/25

3

Source B for Question 2

AG plc uses a system of budgetary control.

The company prepared the following budgets for periods ending March 2026.

1 Sales budget (all on credit)

$

November 96 000

December 88 000

January 102 000

February 100 000

March 92 000

2 Trade receivables budget

January February March

$ $ $

Balance b/f 164 800 172 400 181 600

Sales 102 000 100 000 92 000

266 800 272 400 273 600

Receipts – one month after sale (17 600) (20 400) (20 000)

Receipts – two months after sale (76 800) (70 400) (81 600)

Balance c/f 172 400 181 600 172 000

3 Budgeted statement of financial position at 31 March 2026

$

Non-current assets 426 000

Current assets

Inventory 91 000

Trade receivables 172 000

Total assets 689 000

Equity

Share capital 500 000

Retained earnings 77 320

Current liabilities

Bank overdraft 22 180

Trade payables 89 500

Total equity and liabilities 689 000

© UCLES 2025 9706/42/INSERT/F/M/25

#cambridge#accounting#october-november#may-june#exam-year