9706_w23_in_33

💡 Premium Overlay Enabled

Cambridge International AS

& A Level

ACCOUNTING

9706/33

Paper 3 Financial Accounting

October/November

2023

INSERT

1 hour 30 minutes

* 6 1 1 7 5 6 7 0 0 2 - I *

INFORMATION

●

This insert contains all of the sources referred to in the questions.

●

You may annotate this insert and use the blank spaces for planning.

Do not write your answers

on the

insert.

This document has

4

pages.

DC (PQ) 312027/2

© UCLES 2023

[Turn over

Cambridge International AS & A Level

ACCOUNTING 9706/33

Paper 3 Financial Accounting October/November 2023

INSERT 1 hour 30 minutes

* 6 1 1 7 5 6 7 0 0 2 - I *

INFORMATION

● This insert contains all of the sources referred to in the questions.

● You may annotate this insert and use the blank spaces for planning. Do not write your answers on the

insert.

This document has 4 pages.

DC (PQ) 312027/2

© UCLES 2023 [Turn over

2

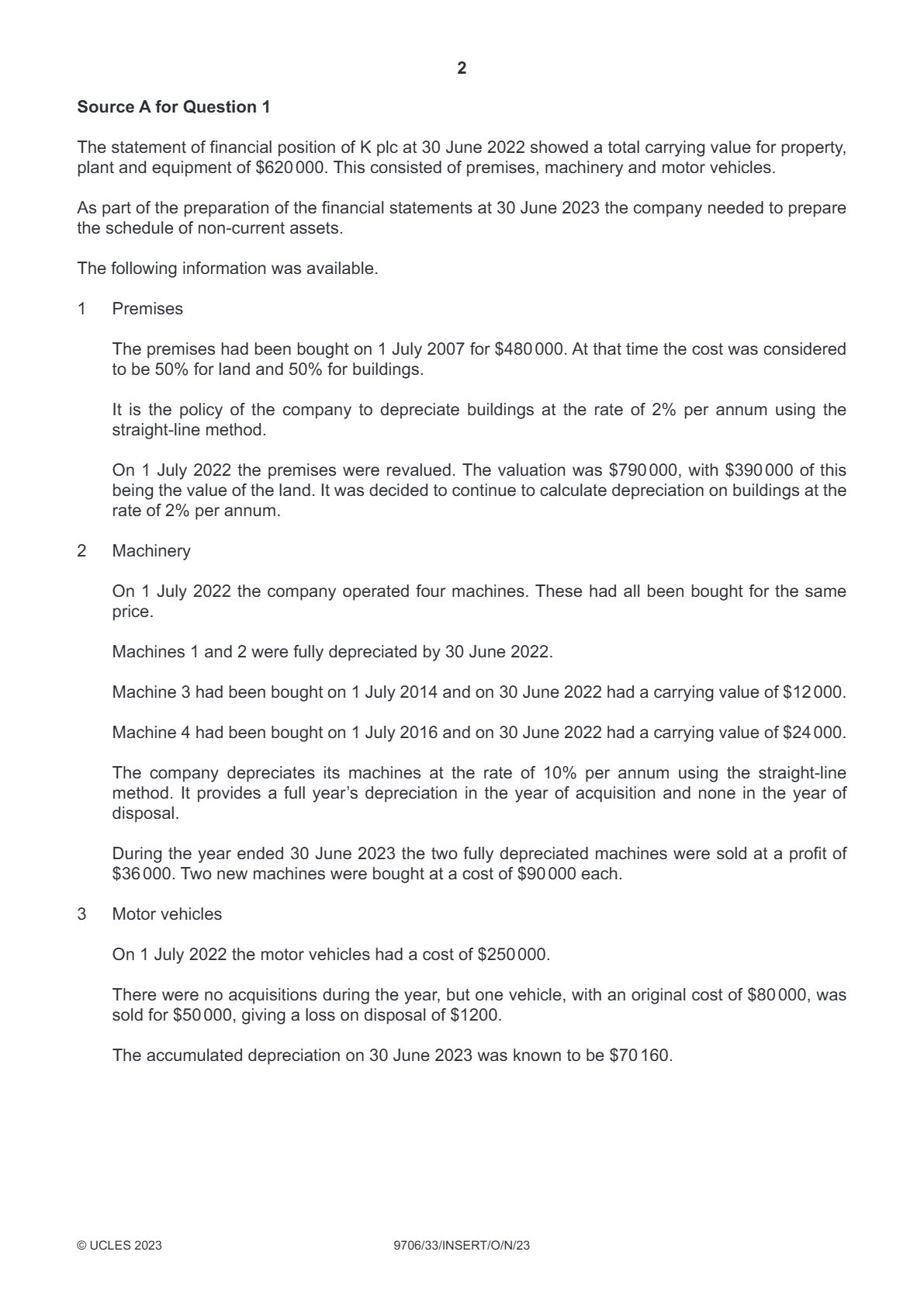

Source A for Question 1

The statement of financial position of K plc at 30 June 2022 showed a total carrying value for property,

plant and equipment of $620 000. This consisted of premises, machinery and motor vehicles.

As part of the preparation of the financial statements at 30 June 2023 the company needed to prepare

the schedule of non-current assets.

The following information was available.

1

Premises

The premises had been bought on 1 July 2007 for $480 000. At that time the cost was considered

to be 50% for land and 50% for buildings.

It is the policy of the company to depreciate buildings at the rate of 2% per annum using the

straight-line method.

On 1 July 2022 the premises were revalued. The valuation was $790 000, with $390 000 of this

being the value of the land. It was decided to continue to calculate depreciation on buildings at the

rate of 2% per annum.

2

Machinery

On 1 July 2022 the company operated four machines. These had all been bought for the same

price.

Machines 1 and 2 were fully depreciated by 30 June 2022.

Machine 3 had been bought on 1 July 2014 and on 30 June 2022 had a carrying value of $12 000.

Machine 4 had been bought on 1 July 2016 and on 30 June 2022 had a carrying value of $24 000.

The company depreciates its machines at the rate of 10% per annum using the straight-line

method. It provides a full year’s depreciation in the year of acquisition and none in the year of

disposal.

During the year ended 30 June 2023 the two fully depreciated machines were sold at a profit of

$36 000. Two new machines were bought at a cost of $90 000 each.

3

Motor vehicles

On 1 July 2022 the motor vehicles had a cost of $250 000.

There were no acquisitions during the year, but one vehicle, with an original cost of $80 000, was

sold for $50 000, giving a loss on disposal of $1200.

The accumulated depreciation on 30 June 2023 was known to be $70 160.

©

UCLES 2023

9706/33/INSERT/O/N/23

2

Source A for Question 1

The statement of financial position of K plc at 30 June 2022 showed a total carrying value for property,

plant and equipment of $620 000. This consisted of premises, machinery and motor vehicles.

As part of the preparation of the financial statements at 30 June 2023 the company needed to prepare

the schedule of non-current assets.

The following information was available.

1 Premises

The premises had been bought on 1 July 2007 for $480 000. At that time the cost was considered

to be 50% for land and 50% for buildings.

It is the policy of the company to depreciate buildings at the rate of 2% per annum using the

straight-line method.

On 1 July 2022 the premises were revalued. The valuation was $790 000, with $390 000 of this

being the value of the land. It was decided to continue to calculate depreciation on buildings at the

rate of 2% per annum.

2 Machinery

On 1 July 2022 the company operated four machines. These had all been bought for the same

price.

Machines 1 and 2 were fully depreciated by 30 June 2022.

Machine 3 had been bought on 1 July 2014 and on 30 June 2022 had a carrying value of $12 000.

Machine 4 had been bought on 1 July 2016 and on 30 June 2022 had a carrying value of $24 000.

The company depreciates its machines at the rate of 10% per annum using the straight-line

method. It provides a full year’s depreciation in the year of acquisition and none in the year of

disposal.

During the year ended 30 June 2023 the two fully depreciated machines were sold at a profit of

$36 000. Two new machines were bought at a cost of $90 000 each.

3 Motor vehicles

On 1 July 2022 the motor vehicles had a cost of $250 000.

There were no acquisitions during the year, but one vehicle, with an original cost of $80 000, was

sold for $50 000, giving a loss on disposal of $1200.

The accumulated depreciation on 30 June 2023 was known to be $70 160.

© UCLES 2023 9706/33/INSERT/O/N/23

3

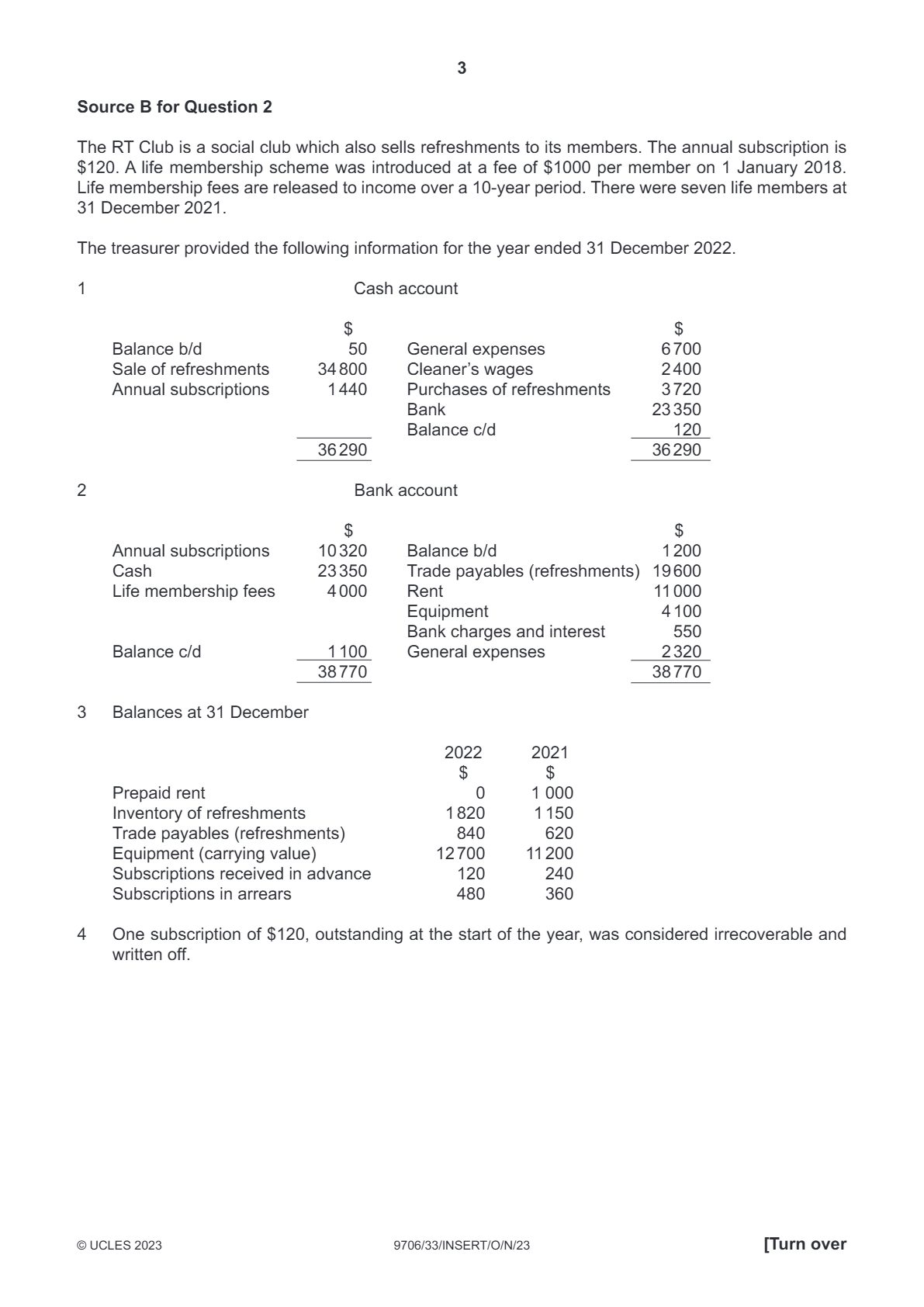

Source B for Question 2

The RT Club is a social club which also sells refreshments to its members. The annual subscription is

$120. A life membership scheme was introduced at a fee of $1000 per member on 1 January 2018.

Life membership fees are released to income over a 10-year period. There were seven life members at

31 December 2021.

The treasurer provided the following information for the year ended 31 December 2022.

1

Cash account

$

$

Balance b/d

50

General expenses

6 700

Sale of refreshments

34 800

Cleaner’s wages

2 400

Annual subscriptions

1 440

Purchases of refreshments

3 720

Bank

23 350

Balance c/d

120

36 290

36 290

2

Bank account

$

$

Annual subscriptions

10 320

Balance b/d

1 200

Cash

23 350

Trade payables (refreshments)

19 600

Life membership fees

4 000

Rent

11 000

Equipment

4 100

Bank charges and interest

550

Balance c/d

1 100

General expenses

2 320

38 770

38 770

3

Balances at 31 December

2022

2021

$

$

Prepaid rent

0

1 000

Inventory of refreshments

1 820

1 150

Trade payables (refreshments)

840

620

Equipment (carrying value)

12 700

11 200

Subscriptions received in advance

120

240

Subscriptions in arrears

480

360

4

One subscription of $120, outstanding at the start of the year, was considered irrecoverable and

written off.

[Turn over

©

UCLES 2023

9706/33/INSERT/O/N/23

3

Source B for Question 2

The RT Club is a social club which also sells refreshments to its members. The annual subscription is

$120. A life membership scheme was introduced at a fee of $1000 per member on 1 January 2018.

Life membership fees are released to income over a 10-year period. There were seven life members at

31 December 2021.

The treasurer provided the following information for the year ended 31 December 2022.

1 Cash account

$ $

Balance b/d 50 General expenses 6 700

Sale of refreshments 34 800 Cleaner’s wages 2 400

Annual subscriptions 1 440 Purchases of refreshments 3 720

Bank 23 350

Balance c/d 120

36 290 36 290

2 Bank account

$ $

Annual subscriptions 10 320 Balance b/d 1 200

Cash 23 350 Trade payables (refreshments) 19 600

Life membership fees 4 000 Rent 11 000

Equipment 4 100

Bank charges and interest 550

Balance c/d 1 100 General expenses 2 320

38 770 38 770

3 Balances at 31 December

2022 2021

$ $

Prepaid rent 0 1 000

Inventory of refreshments 1 820 1 150

Trade payables (refreshments) 840 620

Equipment (carrying value) 12 700 11 200

Subscriptions received in advance 120 240

Subscriptions in arrears 480 360

4 One subscription of $120, outstanding at the start of the year, was considered irrecoverable and

written off.

© UCLES 2023 9706/33/INSERT/O/N/23 [Turn over

#cambridge#accounting#october-november#may-june#exam-year#october/november 2023