9706_w23_in_41

💡 Premium Overlay Enabled

Cambridge International AS

& A Level

ACCOUNTING

9706/41

Paper 4 Cost and Management Accounting

October/November

2023

INSERT

1 hour

* 5 9 5 8 2 4 0 3 9 1 - I *

INFORMATION

●

This insert contains all of the sources referred to in the questions.

●

You may annotate this insert and use the blank spaces for planning.

Do not write your answers

on the

insert.

This document has

4

pages. Any blank pages are indicated.

DC (PQ) 312032/2

© UCLES 2023

[Turn over

Cambridge International AS & A Level

ACCOUNTING 9706/41

Paper 4 Cost and Management Accounting October/November 2023

INSERT 1 hour

* 5 9 5 8 2 4 0 3 9 1 - I *

INFORMATION

● This insert contains all of the sources referred to in the questions.

● You may annotate this insert and use the blank spaces for planning. Do not write your answers on the

insert.

This document has 4 pages. Any blank pages are indicated.

DC (PQ) 312032/2

© UCLES 2023 [Turn over

2

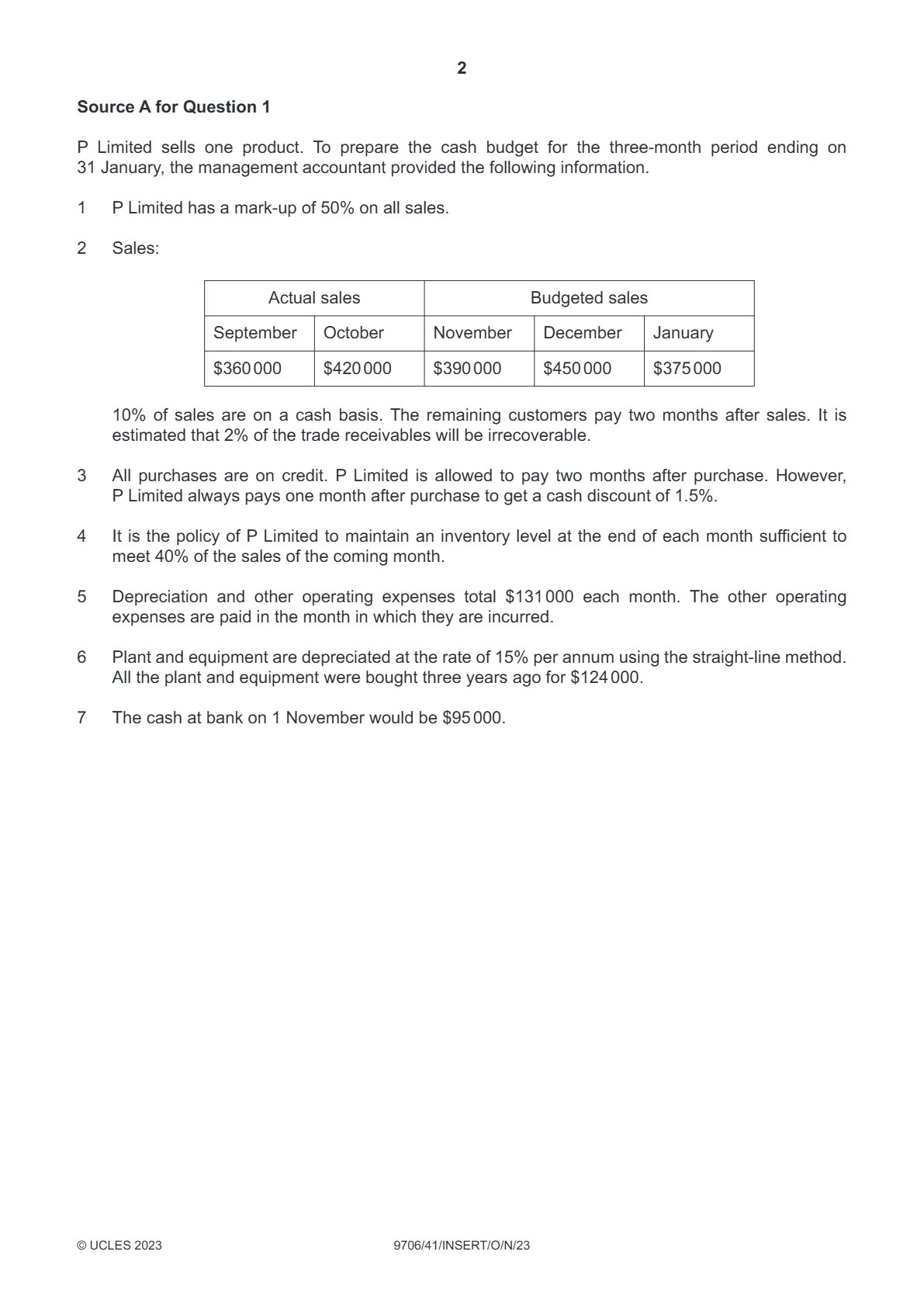

Source A for Question 1

P Limited sells one product. To prepare the cash budget for the three-month period ending on

31 January, the management accountant provided the following information.

1

P Limited has a mark-up of 50% on all sales.

2

Sales:

Actual sales

Budgeted sales

September

October

November

December

January

$360 000

$420 000

$390 000

$450 000

$375 000

10% of sales are on a cash basis. The remaining customers pay two months after sales. It is

estimated that 2% of the trade receivables will be irrecoverable.

3

All purchases are on credit. P Limited is allowed to pay two months after purchase. However,

P Limited always pays one month after purchase to get a cash discount of 1.5%.

4

It is the policy of P Limited to maintain an inventory level at the end of each month sufficient to

meet 40% of the sales of the coming month.

5

Depreciation and other operating expenses total $131 000 each month. The other operating

expenses are paid in the month in which they are incurred.

6

Plant and equipment are depreciated at the rate of 15% per annum using the straight-line method.

All the plant and equipment were bought three years ago for $124 000.

7

The cash at bank on 1 November would be $95 000.

©

UCLES 2023

9706/41/INSERT/O/N/23

2

Source A for Question 1

P Limited sells one product. To prepare the cash budget for the three-month period ending on

31 January, the management accountant provided the following information.

1 P Limited has a mark-up of 50% on all sales.

2 Sales:

Actual sales Budgeted sales

September October November December January

$360 000 $420 000 $390 000 $450 000 $375 000

10% of sales are on a cash basis. The remaining customers pay two months after sales. It is

estimated that 2% of the trade receivables will be irrecoverable.

3 All purchases are on credit. P Limited is allowed to pay two months after purchase. However,

P Limited always pays one month after purchase to get a cash discount of 1.5%.

4 It is the policy of P Limited to maintain an inventory level at the end of each month sufficient to

meet 40% of the sales of the coming month.

5 Depreciation and other operating expenses total $131 000 each month. The other operating

expenses are paid in the month in which they are incurred.

6 Plant and equipment are depreciated at the rate of 15% per annum using the straight-line method.

All the plant and equipment were bought three years ago for $124 000.

7 The cash at bank on 1 November would be $95 000.

© UCLES 2023 9706/41/INSERT/O/N/23

3

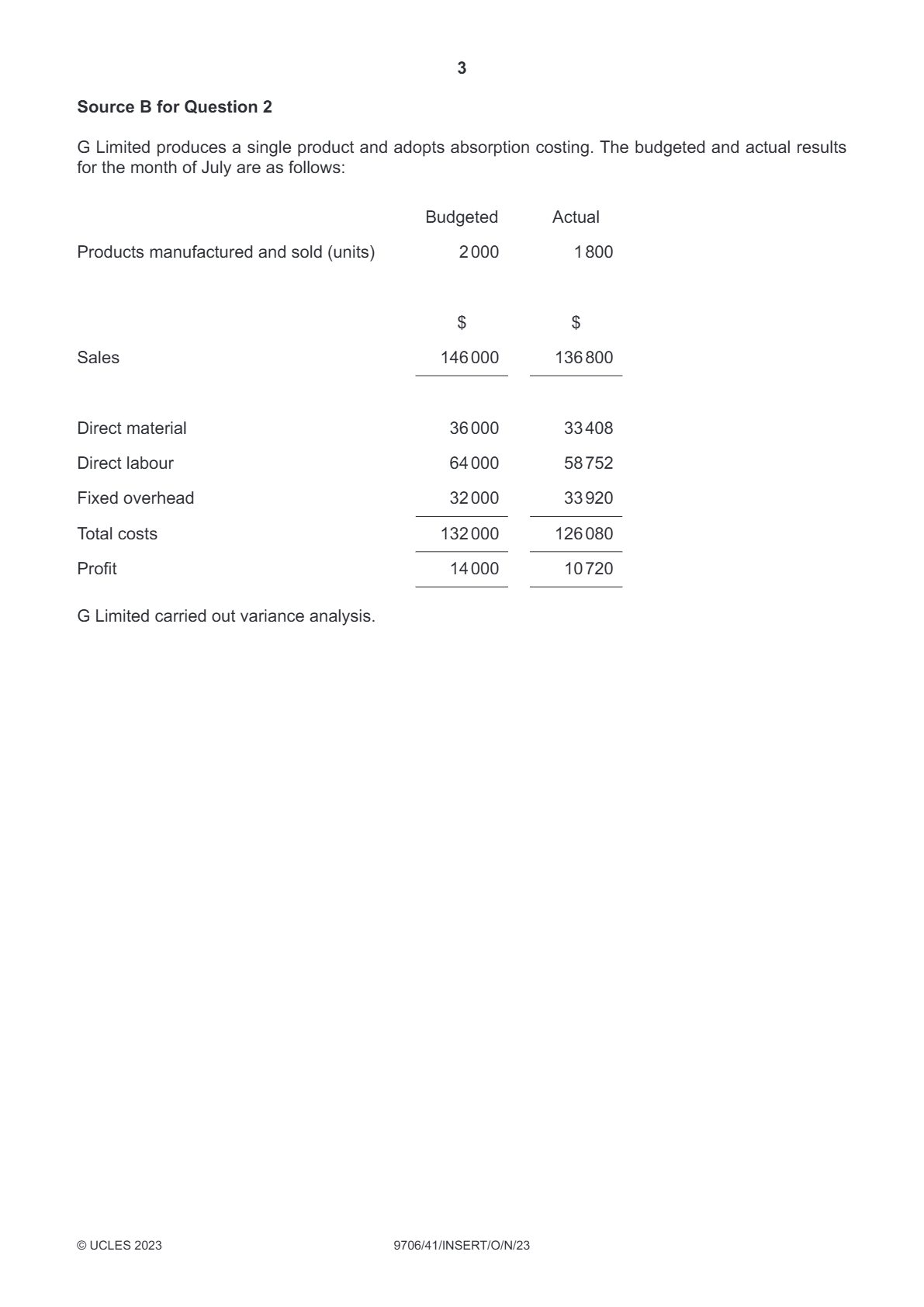

Source B for Question 2

G Limited produces a single product and adopts absorption costing. The budgeted and actual results

for the month of July are as follows:

Budgeted

Actual

Products manufactured and sold (units)

2 000

1 800

$

$

Sales

146 000

136 800

Direct material

36 000

33 408

Direct labour

64 000

58 752

Fixed overhead

32 000

33 920

Total costs

132 000

126 080

Profit

14 000

10 720

G Limited carried out variance analysis.

©

UCLES 2023

9706/41/INSERT/O/N/23

3

Source B for Question 2

G Limited produces a single product and adopts absorption costing. The budgeted and actual results

for the month of July are as follows:

Budgeted Actual

Products manufactured and sold (units) 2 000 1 800

$ $

Sales 146 000 136 800

Direct material 36 000 33 408

Direct labour 64 000 58 752

Fixed overhead 32 000 33 920

Total costs 132 000 126 080

Profit 14 000 10 720

G Limited carried out variance analysis.

© UCLES 2023 9706/41/INSERT/O/N/23

#cambridge#accounting#october-november#may-june#exam-year#october/november 2023