9706_w23_in_42

💡 Premium Overlay Enabled

Cambridge International AS

& A Level

ACCOUNTING

9706/42

Paper 4 Cost and Management Accounting

October/November

2023

INSERT

1 hour

* 3 6 1 2 2 8 4 8 6 5 - I *

INFORMATION

●

This insert contains all of the sources referred to in the questions.

●

You may annotate this insert and use the blank spaces for planning.

Do not write your answers

on the

insert.

This document has

4

pages. Any blank pages are indicated.

DC (PQ) 312036/2

© UCLES 2023

[Turn over

Cambridge International AS & A Level

ACCOUNTING 9706/42

Paper 4 Cost and Management Accounting October/November 2023

INSERT 1 hour

* 3 6 1 2 2 8 4 8 6 5 - I *

INFORMATION

● This insert contains all of the sources referred to in the questions.

● You may annotate this insert and use the blank spaces for planning. Do not write your answers on the

insert.

This document has 4 pages. Any blank pages are indicated.

DC (PQ) 312036/2

© UCLES 2023 [Turn over

2

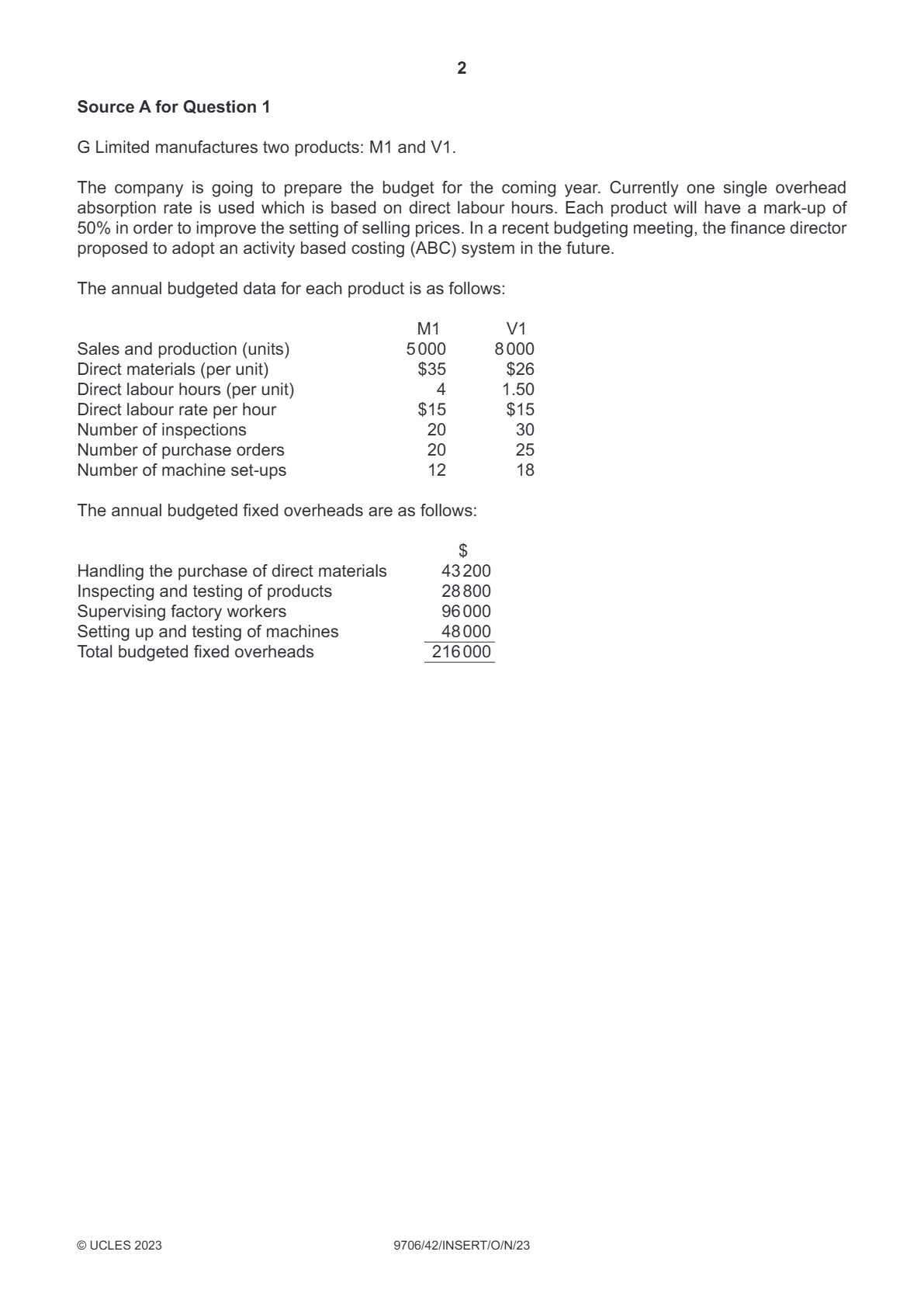

Source A for Question 1

G Limited manufactures two products: M1 and V1.

The company is going to prepare the budget for the coming year. Currently one single overhead

absorption rate is used which is based on direct labour hours. Each product will have a mark-up of

50% in order to improve the setting of selling prices. In a recent budgeting meeting, the finance director

proposed to adopt an activity based costing (ABC) system in the future.

The annual budgeted data for each product is as follows:

M1

V1

Sales and production (units)

5 000

8 000

Direct materials (per unit)

$35

$26

Direct labour hours (per unit)

4

1.50

Direct labour rate per hour

$15

$15

Number of inspections

20

30

Number of purchase orders

20

25

Number of machine set-ups

12

18

The annual budgeted fixed overheads are as follows:

$

Handling the purchase of direct materials

43 200

Inspecting and testing of products

28 800

Supervising factory workers

96 000

Setting up and testing of machines

48 000

Total budgeted fixed overheads

216 000

©

UCLES 2023

9706/42/INSERT/O/N/23

2

Source A for Question 1

G Limited manufactures two products: M1 and V1.

The company is going to prepare the budget for the coming year. Currently one single overhead

absorption rate is used which is based on direct labour hours. Each product will have a mark-up of

50% in order to improve the setting of selling prices. In a recent budgeting meeting, the finance director

proposed to adopt an activity based costing (ABC) system in the future.

The annual budgeted data for each product is as follows:

M1 V1

Sales and production (units) 5 000 8 000

Direct materials (per unit) $35 $26

Direct labour hours (per unit) 4 1.50

Direct labour rate per hour $15 $15

Number of inspections 20 30

Number of purchase orders 20 25

Number of machine set-ups 12 18

The annual budgeted fixed overheads are as follows:

$

Handling the purchase of direct materials 43 200

Inspecting and testing of products 28 800

Supervising factory workers 96 000

Setting up and testing of machines 48 000

Total budgeted fixed overheads 216 000

© UCLES 2023 9706/42/INSERT/O/N/23

3

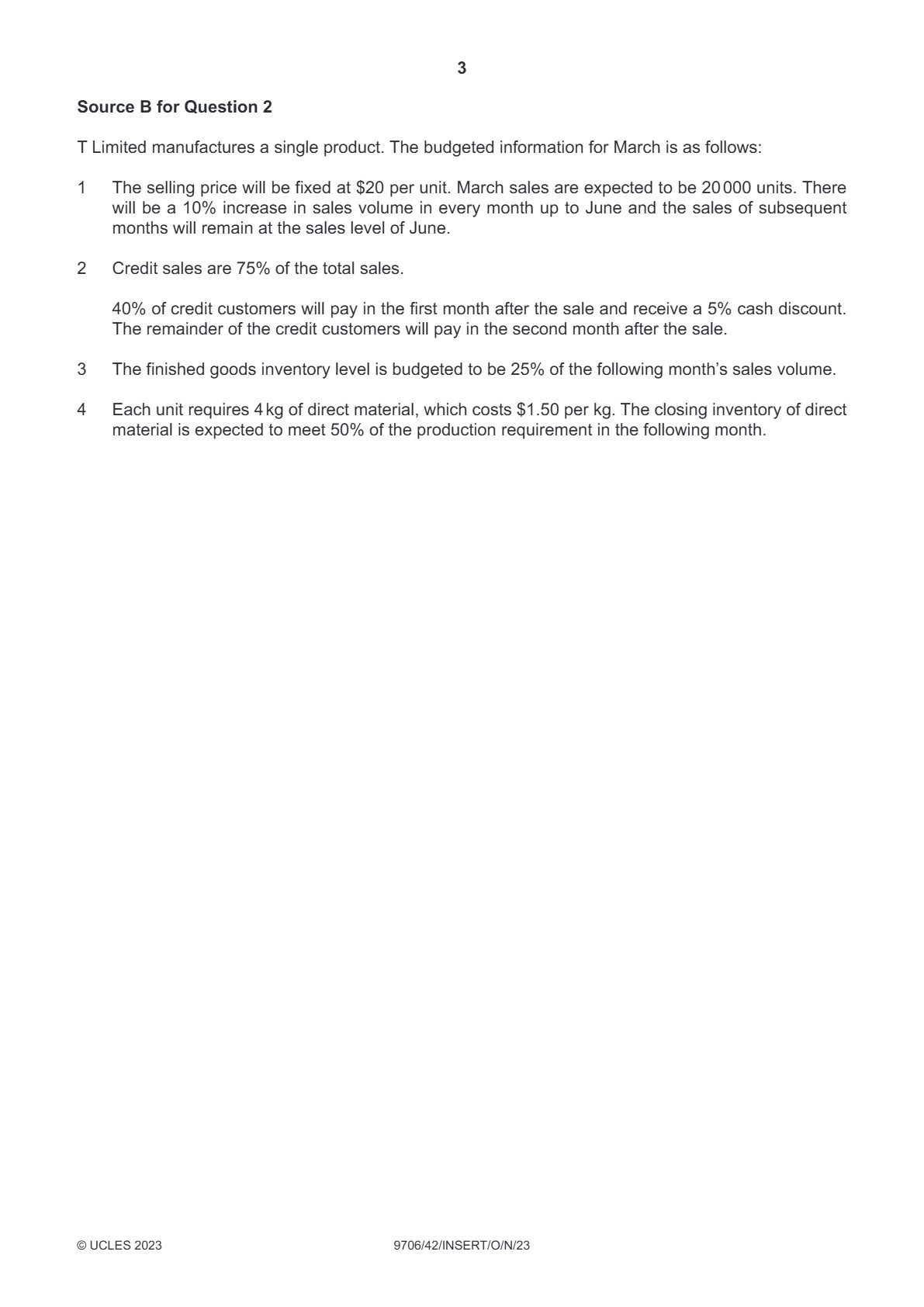

Source B for Question 2

T Limited manufactures a single product. The budgeted information for March is as follows:

1

The selling price will be fixed at $20 per unit. March sales are expected to be 20 000 units. There

will be a 10% increase in sales volume in every month up to June and the sales of subsequent

months will remain at the sales level of June.

2

Credit sales are 75% of the total sales.

40% of credit customers will pay in the first month after the sale and receive a 5% cash discount.

The remainder of the credit customers will pay in the second month after the sale.

3

The finished goods inventory level is budgeted to be 25% of the following month’s sales volume.

4

Each unit requires 4 kg of direct material, which costs $1.50 per kg. The closing inventory of direct

material is expected to meet 50% of the production requirement in the following month.

©

UCLES 2023

9706/42/INSERT/O/N/23

3

Source B for Question 2

T Limited manufactures a single product. The budgeted information for March is as follows:

1 The selling price will be fixed at $20 per unit. March sales are expected to be 20 000 units. There

will be a 10% increase in sales volume in every month up to June and the sales of subsequent

months will remain at the sales level of June.

2 Credit sales are 75% of the total sales.

40% of credit customers will pay in the first month after the sale and receive a 5% cash discount.

The remainder of the credit customers will pay in the second month after the sale.

3 The finished goods inventory level is budgeted to be 25% of the following month’s sales volume.

4 Each unit requires 4 kg of direct material, which costs $1.50 per kg. The closing inventory of direct

material is expected to meet 50% of the production requirement in the following month.

© UCLES 2023 9706/42/INSERT/O/N/23

#cambridge#accounting#october-november#may-june#exam-year#october/november 2023