9706_w23_qp_21

💡 Premium Overlay Enabled

Cambridge International AS

& A Level

* 2 1 6 8 6 0 6 4 0 6 *

ACCOUNTING

9706/21

Paper 2 Fundamentals of Accounting

October/November

2023

1 hour 45 minutes

You must answer on the question paper.

No additional materials are needed.

INSTRUCTIONS

●

Answer

all

questions.

●

Use a black or dark blue pen.

●

Write your name, centre number and candidate number in the boxes at the top of the page.

●

Write your answer to each question in the space provided.

●

Do

not

use an erasable pen or correction fluid.

●

Do

not

write on any bar codes.

●

You may use an HB pencil for any rough working.

●

You may use a calculator.

●

You should present all accounting statements in good style.

●

International accounting terms and formats should be used as appropriate.

●

You should show your workings.

INFORMATION

●

The total mark for this paper is 90.

●

The number of marks for each question or part question is shown in brackets [ ].

This document has

16

pages. Any blank pages are indicated.

DC (LK) 316871/4

© UCLES 2023

[Turn over

Cambridge International AS & A Level

* 2 1 6 8 6 0 6 4 0 6 *

ACCOUNTING 9706/21

Paper 2 Fundamentals of Accounting October/November 2023

1 hour 45 minutes

You must answer on the question paper.

No additional materials are needed.

INSTRUCTIONS

● Answer all questions.

● Use a black or dark blue pen.

● Write your name, centre number and candidate number in the boxes at the top of the page.

● Write your answer to each question in the space provided.

● Do not use an erasable pen or correction fluid.

● Do not write on any bar codes.

● You may use an HB pencil for any rough working.

● You may use a calculator.

● You should present all accounting statements in good style.

● International accounting terms and formats should be used as appropriate.

● You should show your workings.

INFORMATION

● The total mark for this paper is 90.

● The number of marks for each question or part question is shown in brackets [ ].

This document has 16 pages. Any blank pages are indicated.

DC (LK) 316871/4

© UCLES 2023 [Turn over

2

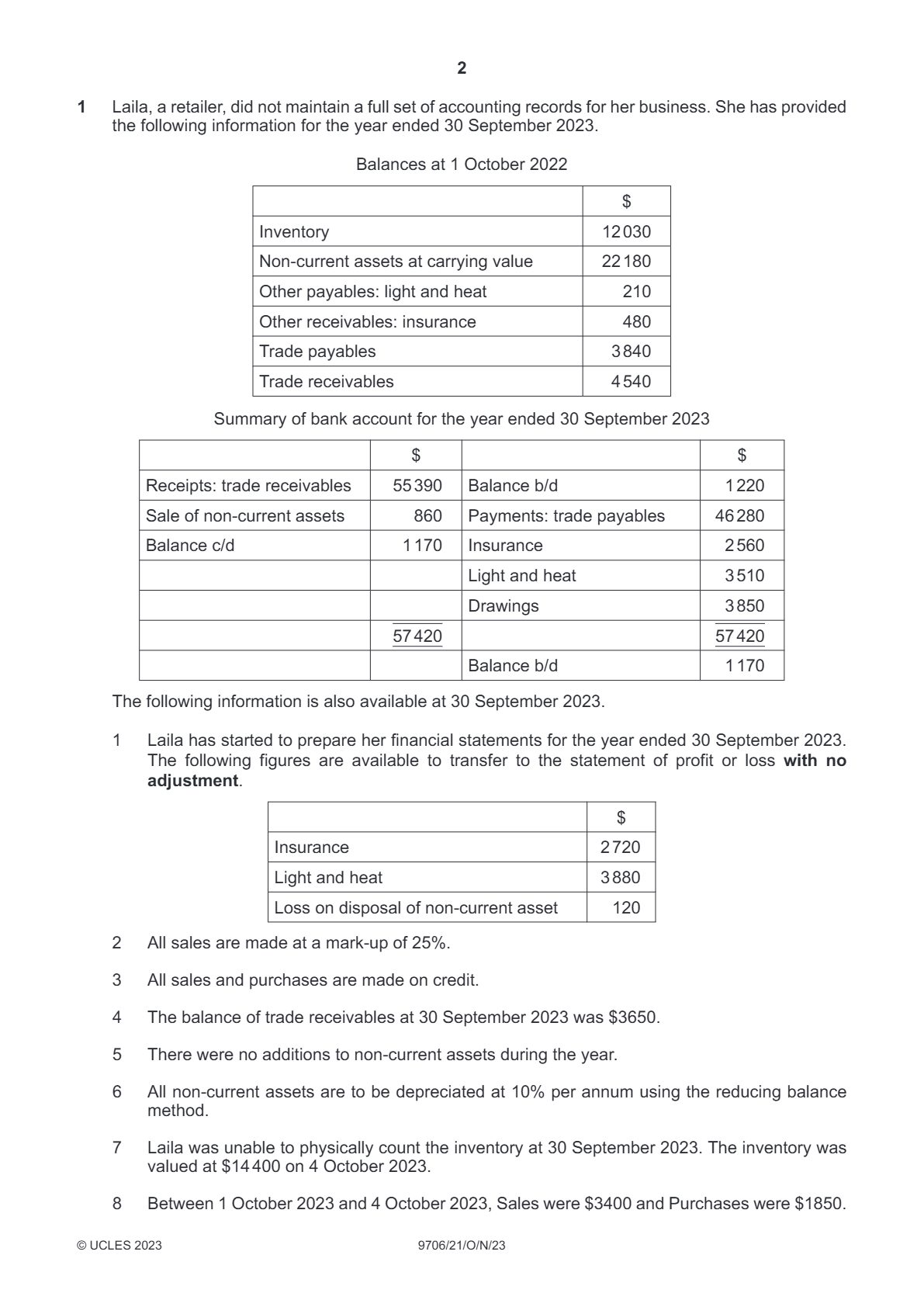

1

Laila, a retailer, did not maintain a full set of accounting records for her business. She has provided

the following information for the year ended 30 September 2023.

Balances at 1 October 2022

$

Inventory

12 030

Non-current assets at carrying value

22 180

Other payables: light and heat

210

Other receivables: insurance

480

Trade payables

3 840

Trade receivables

4 540

Summary of bank account for the year ended 30 September 2023

$

$

Receipts: trade receivables

55 390

Balance b/d

1 220

Sale of non-current assets

860

Payments: trade payables

46 280

Balance c/d

1 170

Insurance

2 560

Light and heat

3 510

Drawings

3 850

57 420

57 420

Balance b/d

1 170

The following information is also available at 30 September 2023.

1

Laila has started to prepare her financial statements for the year ended 30 September 2023.

The following figures are available to transfer to the statement of profit or loss

with no

adjustment

.

$

Insurance

2 720

Light and heat

3 880

Loss on disposal of non-current asset

120

2

All sales are made at a mark-up of 25%.

3

All sales and purchases are made on credit.

4

The balance of trade receivables at 30 September 2023 was $3650.

5

There were no additions to non-current assets during the year.

6

All non-current assets are to be depreciated at 10% per annum using the reducing balance

method.

7

Laila was unable to physically count the inventory at 30 September 2023. The inventory was

valued at $14 400 on 4 October 2023.

8

Between 1 October 2023 and 4 October 2023, Sales were $3400 and Purchases were $1850.

©

UCLES 2023

9706/21/O/N/23

2

1 Laila, a retailer, did not maintain a full set of accounting records for her business. She has provided

the following information for the year ended 30 September 2023.

Balances at 1 October 2022

$

Inventory 12 030

Non-current assets at carrying value 22 180

Other payables: light and heat 210

Other receivables: insurance 480

Trade payables 3 840

Trade receivables 4 540

Summary of bank account for the year ended 30 September 2023

$ $

Receipts: trade receivables 55 390 Balance b/d 1 220

Sale of non-current assets 860 Payments: trade payables 46 280

Balance c/d 1 170 Insurance 2 560

Light and heat 3 510

Drawings 3 850

57 420 57 420

Balance b/d 1 170

The following information is also available at 30 September 2023.

1 Laila has started to prepare her financial statements for the year ended 30 September 2023.

The following figures are available to transfer to the statement of profit or loss with no

adjustment .

$

Insurance 2 720

Light and heat 3 880

Loss on disposal of non-current asset 120

2 All sales are made at a mark-up of 25%.

3 All sales and purchases are made on credit.

4 The balance of trade receivables at 30 September 2023 was $3650.

5 There were no additions to non-current assets during the year.

6 All non-current assets are to be depreciated at 10% per annum using the reducing balance

method.

7 Laila was unable to physically count the inventory at 30 September 2023. The inventory was

valued at $14 400 on 4 October 2023.

8 Between 1 October 2023 and 4 October 2023, Sales were $3400 and Purchases were $1850.

© UCLES 2023 9706/21/O/N/23

3

(a)

Calculate the value of closing inventory at 30 September 2023.

...................................................................................................................................................

...................................................................................................................................................

.............................................................................................................................................

[3]

(b)

Prepare the statement of profit or loss for the year ended 30 September 2023. Use the space

provided on

page 4

to show your workings.

Laila

Statement of profit or loss for the year ended 30 September 2023

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

[Turn over

©

UCLES 2023

9706/21/O/N/23

3

(a) Calculate the value of closing inventory at 30 September 2023.

...................................................................................................................................................

...................................................................................................................................................

............................................................................................................................................. [3]

(b) Prepare the statement of profit or loss for the year ended 30 September 2023. Use the space

provided on page 4 to show your workings.

Laila

Statement of profit or loss for the year ended 30 September 2023

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

...................................................................................................................................................

© UCLES 2023 9706/21/O/N/23 [Turn over

#cambridge#question-paper#accounting#october-november#may-june#exam-year